Definition

From the 2020 financial year, the carry forward rule allows Members to contribute unused concessional contribution cap from up to 5 previous financial years.

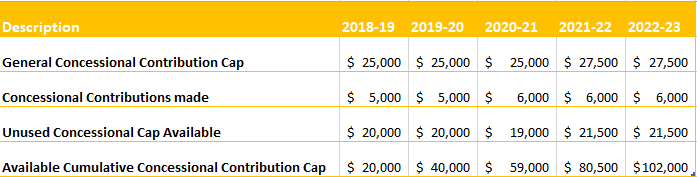

To use your unused cap amounts your total super balance at the end of 30 June of the previous financial year needs to be less than $500,000. You are then able to add unused amounts to your original concessional contributions cap of $25,000 ($27,500 from 1 July 2021).

Example

John is an employee and only receives super guarantee contributions from his employer. John’s super balance is less than $500,000 over the five years. John has a significant unused portion. John could utilise carry-forward concessional contributions to use any of this unused cap by making addition contributions into his super. In financial year 2022/2023, John could make a $102,000 concessional contribution to super on top of the $6,000 he receives from his employer.

The ATO have a full index of listings regarding the concessional contributions cap amount and unused amount. For more information please refer to the ATO website here.

Non-Concessional Contributions

For more information on contributions, please see here for more on non-concessional contributions and the provision regarding the bring forward rule specifically for non-concessional contributions.

We are Melbourne based with clients throughout Australia. Our SMSF administration service is mostly paperless. This enable us to charge a fair fee, resulting in a good value-proposition for you.

Superannuation Warehouse is an accounting firm and do not provide financial advice. All information provided has been prepared without taking into account any of the Trustees’ objectives, financial situation or needs. Because of that, Trustees are advised to consider their own circumstances before engaging our services.

Follow us:

Shop 1/116 Balcombe Rd, Mentone, VIC 3194

03 9583 9813 or 0411 241 215

admin@superannuationwarehouse.com.au

© 2010 - 2023 Superannuation Warehouse : All Rights Reserved

Digital Strategy by